A UAE company can be fast to form, but building a robust corporate structure takes more than picking a license and a free zone. The decisions you make at setup affect everything that follows: who controls what, how profits move, how banking works, what you must file each year, and how exposed you are to regulatory and commercial risk.

This guide breaks down how to design a corporate structure in the UAE that is clear, compliant, and built to scale, without overengineering it.

What “corporate structure” means in the UAE (and why it matters)

In practical terms, your corporate structure is the full blueprint of:

- Entity type and jurisdiction (mainland, free zone, offshore, financial free zone)

- Ownership and control (shareholders, voting rights, reserved matters)

- Governance (directors/managers, decision-making, documented resolutions)

- Regulatory footprint (tax, VAT, UBO, AML where relevant, reporting obligations)

- Operational substance (people, premises, contracts, invoicing flows)

- Banking and payments (account eligibility, KYC narrative, transaction flows)

A robust structure is one that:

- matches your real business model (not a template)

- is understandable to banks, auditors, and counterparties

- reduces avoidable tax and compliance risk

- can scale (new shareholders, new markets, new entities) with minimal disruption

Start with the “why”: the four drivers that should shape your structure

Before choosing a jurisdiction or drafting constitutional documents, define the drivers that will constrain (and simplify) the right answer.

1) Where will you trade, and with whom?

If you will sign contracts with UAE mainland customers, hire staff locally, or require certain regulated activities, your structure may need a mainland presence or specific approvals. If most revenue is international, a free zone entity may be appropriate, depending on activity and operational needs.

2) How important is banking speed and resilience?

Banking is often the critical path. A clean ownership story, clear source of funds, coherent expected activity, and well-documented governance typically reduce friction during KYC and ongoing reviews.

3) Will you raise capital, add partners, or exit?

If you plan to bring investors, create employee incentives, or sell the business later, you need an ownership and governance model that supports:

- predictable decision-making

- minority protections (when needed)

- clean cap table logic

- straightforward due diligence

4) What is your tax and reporting profile?

The UAE has federal corporate tax (with specific rules and exceptions) and VAT for relevant businesses. A structure that looks “simple” on paper can become costly if it creates avoidable filings, unclear transfer pricing positions, or weak documentation.

For official references, see the UAE Ministry of Finance corporate tax hub and guidance via the UAE Ministry of Finance, and VAT information via the Federal Tax Authority.

Core UAE setup options (and where each fits)

The UAE offers several ways to incorporate and operate. The right choice depends on where you trade, what you do, and how you need to present to banks and counterparties.

Mainland entity

A mainland company (often an LLC) is typically used when you need broad access to the UAE market and local contracting flexibility.

Free zone entity

Free zone companies are popular for international trading, services, holding activities, and operational setups that benefit from free zone ecosystems. Rules vary widely by free zone, so the “best” choice is rarely universal.

Offshore entity

Offshore entities are usually used for holding assets or specific structuring objectives rather than running operating businesses with staff and day-to-day UAE activities. Banking and substance expectations should be assessed early.

Financial free zones (ADGM, DIFC)

These jurisdictions have their own company frameworks and are often used for holding structures, investment vehicles, and certain regulated activities. They can be attractive where common-law style documentation and governance are important, but they are not automatically the best fit for every SME.

Quick comparison table

| Option | Best for | Common watch-outs | Typical structuring use |

|---|---|---|---|

| Mainland | Broad UAE market access, local contracting | Licensing scope, compliance workload, cost structure | Operating company that sells into the UAE |

| Free zone | International business, ecosystem support | Activity limitations, substance expectations, varying rules | Operating company, IP/holding in some cases |

| Offshore | Asset holding, specific ownership arrangements | Banking friction, limited “operating” profile | Passive holding company (case-dependent) |

| ADGM/DIFC | Investment/holding, complex governance needs | Cost, admin rigor, suitability | Holding/SPV, group governance layer |

Build the structure like an engineer: a practical 6-layer model

Robust structuring is easiest when you separate decisions into layers. Each layer should support the one above it.

Layer 1: Map your activities precisely

Licensing is not a formality. Your activity description influences approvals, banking comfort, invoicing logic, and compliance obligations.

Aim for language that is:

- accurate (what you actually do)

- scalable (what you will do in 12 to 24 months)

- defensible to a bank KYC team

Layer 2: Choose the jurisdiction that matches your operating reality

Rather than starting with “mainland vs free zone,” start with operational facts:

- Will you need a UAE office lease immediately?

- Will you hire staff in the UAE?

- Will you sign a large number of local customer contracts?

- Will you rely on payment processors or platforms with strict onboarding?

A jurisdiction should reduce friction across those requirements, not create exceptions you constantly need to manage.

Layer 3: Design ownership and control (shareholders, voting, and protections)

Ownership is not only about percentage shareholding. A resilient structure clarifies:

- who controls day-to-day decisions

- which decisions require special approvals (for example, issuing shares, borrowing, selling key assets)

- how profits are distributed

- what happens if a shareholder exits or passes away

In many cases, this is addressed through a combination of constitutional documents plus a shareholders’ agreement (where appropriate).

Layer 4: Put governance on paper (and keep it current)

Governance is one of the fastest ways to look “real” to banks and counterparties, and one of the easiest areas to neglect.

At minimum, build a system for:

- director/manager appointments and acceptance

- documented resolutions for key decisions

- clear signing authority (and internal approval rules)

- well-organized corporate records

If you plan to operate as a group (multiple entities), governance should also specify how intercompany agreements are approved and signed.

Layer 5: Engineer compliance so it runs in the background

A robust corporate structure is compliant by design. Typical UAE compliance areas include:

- UBO (Ultimate Beneficial Owner) disclosure and maintaining up-to-date registers (see the UAE Ministry of Economy’s overview on beneficial owner procedures)

- Corporate tax registration, assessments, and documentation where applicable (see UAE Ministry of Finance)

- VAT registration and filings if thresholds and rules apply (see Federal Tax Authority)

- Accounting and bookkeeping that matches the reality of your transactions (especially if you have multiple revenue lines)

The best time to decide who owns each compliance responsibility is before incorporation, not after the first deadline is missed.

Layer 6: Make banking and payment flows consistent with the story

Banks want a coherent narrative: who you are, what you do, where money comes from, where it goes, and why.

Common pitfalls that undermine robustness:

- mismatched license activity vs invoices/contracts

- unclear shareholder source of funds narrative

- complicated intercompany transfers without documentation

- weak governance evidence (no resolutions, unclear authority)

If you will have a group structure, document intercompany relationships early (service agreements, cost sharing, IP licensing where relevant). Do not backfill this when a bank asks.

Common “robust structure” patterns (and when to use them)

The best structure is the one you can operate and explain. These are common patterns that can work well when they match the business reality.

1) Single-entity operating company (the simplicity-first option)

Ideal when:

- you have one line of business

- you do not need ring-fencing

- you are pre-funding and want faster administration

Robustness here comes from governance, clean bookkeeping, and correct licensing, not from adding entities.

2) Holding company plus operating company (control and risk separation)

Ideal when:

- you want to separate ownership from operations

- you may add more operating subsidiaries later

- you want cleaner investor entry/exit at the holdco level

This can also support succession planning, but only if the governance and documentation are maintained properly.

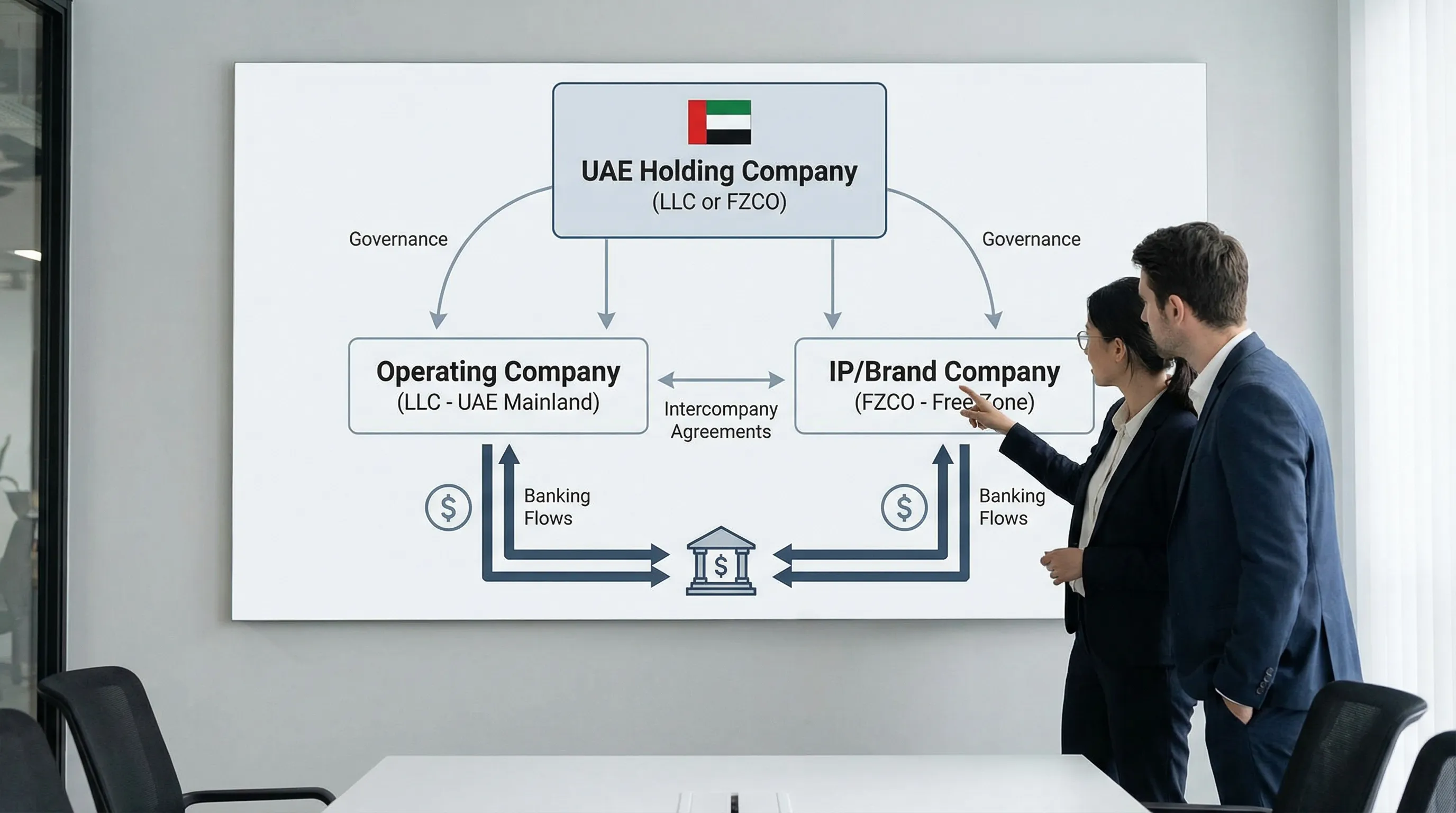

3) UAE group with function-based entities (only when there is real substance)

Examples include separating an operating company from a brand/IP company or a regional contracting entity.

This pattern can make sense when:

- there is genuine operational separation

- contracts, people, and decision-making match the split

- intercompany agreements and pricing are documented and defensible

If the split is only “on paper,” it often creates more compliance, banking questions, and tax documentation burden than value.

A governance and compliance checklist you can actually use

Use this as a practical benchmark for what “robust” looks like after setup.

| Area | Minimum standard for robustness | Why it matters |

|---|---|---|

| Ownership records | Clear shareholder register and UBO information kept current | Supports regulatory compliance and bank KYC |

| Signing authority | Documented authority rules and consistent signing practice | Reduces contract disputes and internal risk |

| Resolutions | Written resolutions for key actions (bank accounts, major contracts, borrowing) | Improves auditability and credibility |

| Accounting | Regular bookkeeping aligned to contracts and invoices | Enables correct tax/VAT position and reporting |

| Tax readiness | Corporate tax and VAT assessed early, registrations handled when required | Avoids penalties and last-minute restructuring |

| Document control | Organized corporate records with version control | Makes due diligence and banking reviews easier |

Mistakes that quietly weaken a UAE corporate structure

Even well-intentioned founders run into these issues.

Treating incorporation as the finish line

Incorporation is the start. A structure becomes robust when it is operated consistently: contracts, invoicing, approvals, and compliance should match the original design.

Choosing a jurisdiction before defining the operating model

If you pick a free zone (or mainland) based on a trend, you can end up with workarounds that complicate banking and contracting.

Overbuilding (too many entities too early)

Extra entities mean extra accounts, extra filings, extra intercompany documentation, and more governance. Add complexity only when it creates clear benefits.

Under-documenting intercompany and shareholder arrangements

If money moves between related parties, or if partners have side agreements, document it. Missing documents tend to surface during banking onboarding, audits, or disputes.

When to bring in experts (and what to ask them)

You usually need expert input when:

- you are setting up a group or holding structure

- you have international shareholders or complex source of funds

- you plan to raise capital, issue different share classes, or bring in key partners

- you have regulated activities or unusual revenue flows

Questions worth asking your advisor:

- “Can you explain this structure in one page for a bank KYC team?”

- “What are the ongoing compliance tasks, and who owns each one?”

- “What changes if we add a new shareholder or a second operating line?”

- “What documentation will we need to defend intercompany payments?”

Frequently Asked Questions

What is a corporate structure in the UAE? A corporate structure is how your UAE business is legally organized: the entity type and jurisdiction, ownership and control, governance (directors/managers), and the compliance and banking setup that supports operations.

Is a free zone company always the best option for a UAE corporate structure? No. Free zones can be excellent for many international and service businesses, but the best option depends on where you trade, licensing needs, hiring plans, and banking requirements.

Do I need a holding company to build a robust corporate structure in the UAE? Not always. A single operating entity can be very robust if licensing, governance, documentation, and compliance are done properly. A holding company is most useful when you need risk separation, investor flexibility, or a scalable group model.

What makes a UAE corporate structure “bank-friendly”? Clear ownership and UBO details, a license that matches real activity, consistent contracts and invoicing, documented governance (resolutions and authority), and a coherent source of funds and transaction-flow narrative.

How do corporate tax and VAT affect UAE structuring? They influence how you document revenue and costs, whether registrations are required, and how intercompany arrangements should be set up. Always assess tax and VAT early so your structure remains compliant as you grow.

Build a robust UAE corporate structure with Alldren

If you want a UAE corporate structure that is built to last, the goal is clarity: the right entity setup, clean governance, and a compliance model you can run without constant firefighting.

Alldren provides expert-led, transparent support for company setup and structuring, ongoing compliance management, corporate governance, bank account opening support, and related corporate services in the UAE. Explore options at Alldren and speak with a senior expert to design a structure that fits your business, not just the paperwork.

This article is general information and not legal or tax advice.