A company holding structure can be one of the cleanest ways to own multiple UAE and international businesses, ring fence risk, and make future investment or exit easier. It can also become an expensive, compliance-heavy layer that adds little value if your business is simple.

This guide explains when a company holding structure in the UAE works, what it typically looks like in practice, and the tax, banking, and governance realities to consider in 2026.

What “holding structure” means in the UAE (and what it is not)

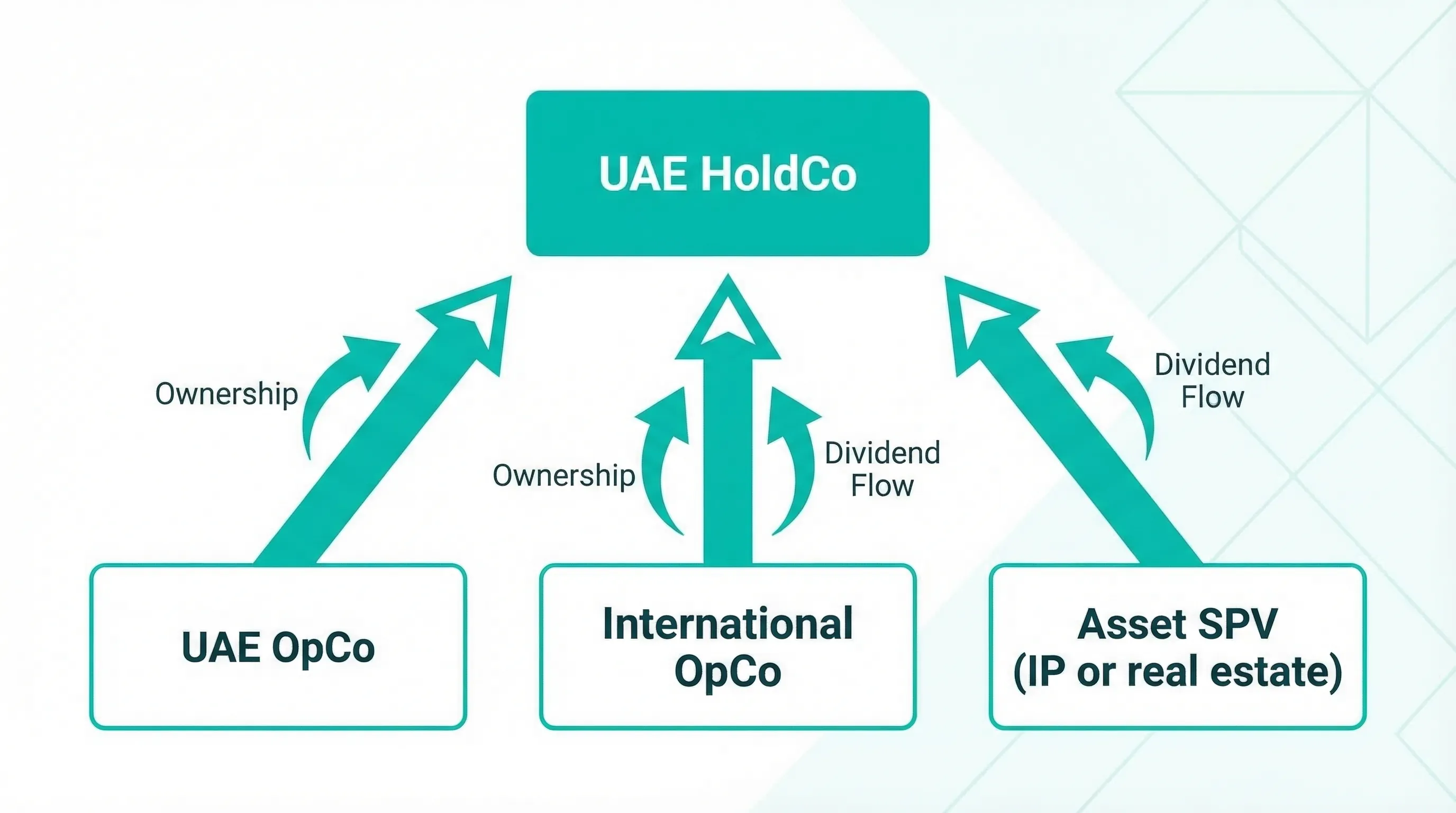

A holding structure is a group setup where a HoldCo (holding company) owns shares in one or more operating companies (OpCos) or asset-owning entities.

In a UAE context, the HoldCo is often used to:

- Own one or more UAE mainland or free zone OpCos

- Own non-UAE subsidiaries

- Hold assets like IP, brand rights, or real estate (often via separate SPVs)

- Centralize shareholder control and governance

What it is not: a “paper company” that automatically reduces tax or eliminates compliance. Since the introduction of UAE Corporate Tax (effective for financial years starting on or after 1 June 2023), group structures need to be built with real commercial reasoning, proper documentation, and ongoing compliance.

The most common UAE holding structure patterns

There is no single “best” template, but in practice you will see a few patterns repeated.

Pattern A: HoldCo above multiple UAE operating companies

Used when you have (or plan to have) more than one licensed activity, brand, or line of business.

Example: A trading entity and a services entity, each with different licensing, risk, or staffing needs, owned by one HoldCo.

Pattern B: HoldCo for investor readiness

Used when you want a clean cap table at the top, and subsidiaries below it.

Example: Investors buy into the HoldCo, while the OpCos remain operationally stable.

Pattern C: HoldCo plus SPVs for assets

Used when you want to separate operating risk from valuable assets.

Example: An OpCo signs customer contracts, while an SPV owns IP (or a real estate asset) and licenses it under a documented arrangement.

Pattern D: UAE HoldCo for an international group

Used when UAE becomes a regional HQ, treasury hub, or control center.

Example: UAE HoldCo owns subsidiaries in multiple jurisdictions, supported by group governance, finance, and bankability.

When a company holding structure in the UAE works best

A holding structure is most effective when it solves a real business problem. These are the scenarios where it usually adds clear value.

1) You are building a multi-entity group (now or within 12 to 24 months)

If you expect multiple subsidiaries, acquisitions, or spin-ups, a HoldCo can avoid repeated restructuring later.

Typical triggers:

- Launching new verticals with separate risk profiles

- Buying into existing businesses (minority or majority)

- Adding regulated or higher-liability activities

2) You need stronger risk segregation

Holding structures help separate liabilities.

Common use cases:

- Customer-contracting entity separated from an asset-owning entity

- Separation between a “high volume, lower margin” OpCo and a “high value, higher risk” OpCo

- Containing risk in one subsidiary without endangering the rest of the group

This is not a substitute for good contracts and insurance, but it is a meaningful layer of corporate risk design.

3) You want flexibility for selling one business line

If you may sell one subsidiary without selling the whole group, a HoldCo structure can keep things clean.

Instead of selling “a business,” you may sell shares in a specific subsidiary (subject to legal, regulatory, and tax considerations). That typically reduces the operational disruption of a sale.

4) You plan to bring in investors or partners

Investors usually prefer:

- A clear ownership story

- Clean governance

- Separation between shareholder-level decisions and operational execution

A HoldCo can centralize shareholder agreements, board composition, reserved matters, and dividend policy, while allowing each OpCo to run day-to-day.

5) You need a structured approach to profit distribution across the group

For groups with multiple entities, holding structures can simplify how profits move (for example, via dividends or documented intercompany arrangements).

This matters because banks, auditors, and tax authorities increasingly expect flows to be understandable and supportable.

6) You are doing succession or family governance planning

For families and private clients, a HoldCo can create a single “control point” for:

- Family governance and voting rights

- Succession arrangements (often alongside professional estate planning)

- Consolidated reporting across assets

7) You have genuine HQ functions in the UAE

If the UAE entity is not just a shareholder, but also provides real group direction (strategy, finance, oversight, management services), a holding structure aligns better with reality.

Practically, this can help with bankability and long-term credibility, especially when paired with proper governance and documentation.

When a holding structure often does not work (or is premature)

A UAE holding structure can be the wrong tool when it adds complexity without delivering a tangible benefit.

You only have one straightforward business

If you run a single OpCo, with one activity, one revenue line, and no near-term plans for subsidiaries or external investors, a HoldCo layer often becomes “admin overhead.”

You are trying to solve a tax problem without commercial substance

A structure that exists mainly “for tax” tends to fail under scrutiny, whether from banks (KYC), auditors, or tax authorities. The UAE has a clear corporate tax framework and transfer pricing expectations, and the direction globally is toward substance and documentation.

For official starting points, see the UAE Ministry of Finance corporate tax overview and the Federal Tax Authority resources.

You are not ready for ongoing compliance

A holding structure usually means:

- More accounting

- More corporate maintenance

- More governance decisions and documentation

- More bank accounts and KYC renewals

If your team is lean and you need speed, simplification can be the better strategy.

A quick decision framework

Use this as a practical filter before designing a group structure.

| Question | If “Yes” | If “No” |

|---|---|---|

| Will you have 2+ operating entities within ~24 months? | A HoldCo can reduce future restructuring. | Keep it simple until expansion is real. |

| Do you need to ring fence valuable assets from operational risk? | Consider HoldCo plus asset SPVs. | A single OpCo may be sufficient. |

| Do you expect external investors, a JV, or a partial sale? | HoldCo improves cap table clarity and deal hygiene. | Structure for operational efficiency first. |

| Are intercompany cashflows likely (dividends, funding, management services)? | HoldCo can centralize treasury and governance. | Avoid complexity unless needed. |

| Can you maintain proper documentation and compliance? | Structure is more likely to be sustainable. | Delay the HoldCo or outsource the function. |

Corporate tax and compliance realities to consider in 2026

A holding structure is not only a legal diagram, it is a compliance system. Key areas to model early:

UAE Corporate Tax, group income, and documentation

UAE Corporate Tax is generally applied at 9 percent on taxable income above the applicable threshold (with rules and definitions set by law and guidance). Holding companies may benefit from certain regimes and exemptions in specific circumstances, but these are condition-based and need careful review.

Examples of topics that often matter for holding structures:

- Participation-type exemptions on certain dividend income or gains, subject to conditions

- Free zone regimes, where a qualifying free zone person may access a 0 percent rate on qualifying income, subject to detailed requirements

- Transfer pricing and related-party documentation for intercompany transactions (management fees, IP royalties, loans)

Because eligibility and conditions depend on facts, you should validate the intended flows with corporate tax guidance and professional advice.

Substance and “real-world” operating footprint

Even where a holding company’s activity is primarily shareholding, banks and counterparties often expect:

- A clear business rationale

- Identifiable decision-makers (directors, managers)

- Evidence of governance and oversight

- Accurate books, records, and financial statements

The separate Economic Substance Regulations (ESR) regime was repealed, but in practice, the concept of “substance” still shows up through tax, banking, and commercial diligence.

Governance and compliance stack

A UAE holding structure typically needs:

- Proper corporate governance (board resolutions, shareholder resolutions)

- UBO and AML-related filings where applicable

- Accounting and, in some cases, audit (depending on jurisdiction and license requirements)

- A compliance calendar across all entities

If you plan nominee arrangements, treat governance even more carefully. Nominee director services can be legitimate in specific scenarios, but they increase the importance of documented control, responsibilities, and ongoing oversight.

Choosing the right place for the HoldCo (mainland vs free zone vs financial centers)

The best jurisdiction depends on what the HoldCo will do, what it will own, and how the group operates.

Here is a practical comparison of common options (high level, not exhaustive):

| HoldCo option | Typical fit | Key considerations |

|---|---|---|

| UAE mainland company | Groups needing broad onshore flexibility | Licensing scope, office/lease expectations, and how it interacts with your OpCos and contracts |

| UAE free zone company | Groups that want a straightforward corporate base and free zone ecosystem | Free zone rules, whether you need to trade onshore, and corporate tax treatment based on your facts |

| ADGM entity (incl. SPV frameworks) | Holding shares or assets in a common law environment | Specific eligibility, ongoing requirements, and setup costs; review official ADGM guidance |

| DIFC entity (incl. prescribed company options) | Structured holdings and group entities within DIFC’s legal framework | Eligibility and requirements under DIFC; confirm the intended use case fits |

Reference points:

A practical rule: pick the HoldCo location based on governance, banking, and how ownership and funds must move, not on marketing claims.

Banking and cash management: where holding structures succeed or stall

Many UAE holding structures look perfect on paper and then slow down at the bank account stage.

Holding company banking often requires extra clarity on:

- Source of funds and source of wealth (especially for shareholder-funded groups)

- Group chart and ownership documentation

- Commercial rationale for each entity

- Nature of expected transactions (dividends, intercompany funding, management fees)

To reduce friction, plan the banking story early and align it with the legal and accounting reality. Also ensure intercompany arrangements are documented before money starts moving.

Implementing a holding structure cleanly (without over-engineering)

A good structure is understandable, maintainable, and aligned with operations. In most cases, implementation works best when you start with a short “structure blueprint” and then build.

Common implementation components:

- Group map: entities, owners, jurisdictions, and purpose of each company

- Asset mapping: what must be protected or separated (IP, contracts, real estate)

- Governance design: board composition, reserved matters, signing authority

- Intercompany documents: funding agreements, service agreements, IP licensing (where applicable)

- Accounting model: how revenue, costs, and intercompany charges will be recorded

- Compliance calendar: tax registrations, filings, renewals, and reporting

If you do not need SPVs, do not add them “just in case.” Every additional entity increases maintenance, documentation, and the chance of inconsistency.

Common pitfalls (and how to avoid them)

Building the HoldCo first, without designing cashflows

If you do not define how money will move (dividends, loans, fees), you may end up with blocked cash, bank delays, or avoidable tax complexity.

Charging intercompany fees without support

Management fees, royalties, and intercompany interest need a clear rationale and documentation. In a corporate tax environment, transfer pricing principles matter, even for closely held groups.

Mixing personal spending with holding structures

This creates audit, banking, and tax risk quickly. Treat the HoldCo like a real corporate body with governance discipline.

Choosing a jurisdiction based only on “ease”

Fast setup can be appealing, but a holding company is a long-term control layer. Optimize for sustainability, compliance, and bankability.

Where Alldren fits if you are considering a UAE holding structure

A holding structure is not a template, it is an engineered system across licensing, governance, tax registration, banking support, and ongoing compliance.

If you want a second opinion before you add complexity, Alldren provides expert-led, transparent support for UAE company setup, structuring, and ongoing compliance, with direct access to senior experts. You can start by outlining your goals and current group on the Alldren website and validating whether a HoldCo is the right next step, or whether a simpler structure will serve you better for now.