Opening a corporate bank account in the UAE can feel deceptively simple until you hit the real gatekeeper: bank-specific compliance. Two companies with the same trade license can get completely different outcomes depending on the bank’s risk appetite, the ownership structure, and how clearly the business activity is documented.

This guide breaks down corporate bank account in UAE requirements by bank type, so you can prepare the right evidence the first time and reduce delays, back-and-forth, or outright rejections.

Why UAE bank requirements vary so much

UAE banks operate under a strong compliance framework and have to make their own risk decisions on top of the baseline rules. In practice, requirements differ because of:

- Risk-based AML/KYC policies (banks must identify customers, beneficial owners, and the source of funds and wealth).

- Industry exposure (some banks are conservative on activities like certain trading models, crypto-related services, or complex cross-border flows).

- Client profile (newly formed companies, non-resident owners, and holding structures often face higher scrutiny).

- Operational “substance” (proof you are a real operating business, not just a paper entity).

For reference, UAE AML obligations are anchored in the country’s AML framework and supervisory expectations, including guidance published by the UAE Central Bank and related competent authorities (see the Central Bank of the UAE for official resources).

Universal requirements (what almost every bank will ask for)

Regardless of bank type, you should assume you will need a clean, consistent set of corporate documents and personal KYC for all relevant individuals.

Core corporate documents

Most UAE banks request some version of the following:

| Document | Who provides it | What the bank checks |

|---|---|---|

| Trade license (Mainland or Free Zone) | Issuing authority / company | Activity matches the account purpose and expected transactions |

| Certificate of incorporation / registration | Issuing authority / company | Legal existence and registration details |

| Memorandum and Articles of Association (MOA/AOA) | Company | Share capital, ownership, powers of signatories |

| Share certificate(s) and shareholder register | Company | Ownership chain and percentages |

| UBO declaration and ownership chart | Company | Ultimate beneficial owners, control, complexity of structure |

| Board resolution (account opening, signatories) | Company | Clear authority and signing rules |

| Office lease / Ejari or Free Zone flexi-desk proof (if applicable) | Company | Physical presence and operational footprint |

| Website and company profile | Company | Commercial credibility, consistency with license |

Personal KYC for owners and signatories

Banks commonly ask for:

- Passport copy (and entry stamp if applicable)

- UAE visa and Emirates ID (if resident, some banks also onboard non-residents with additional checks)

- Proof of address (often recent utility bill or equivalent)

- CV or professional background summary (especially for regulated, financial, or higher-risk activities)

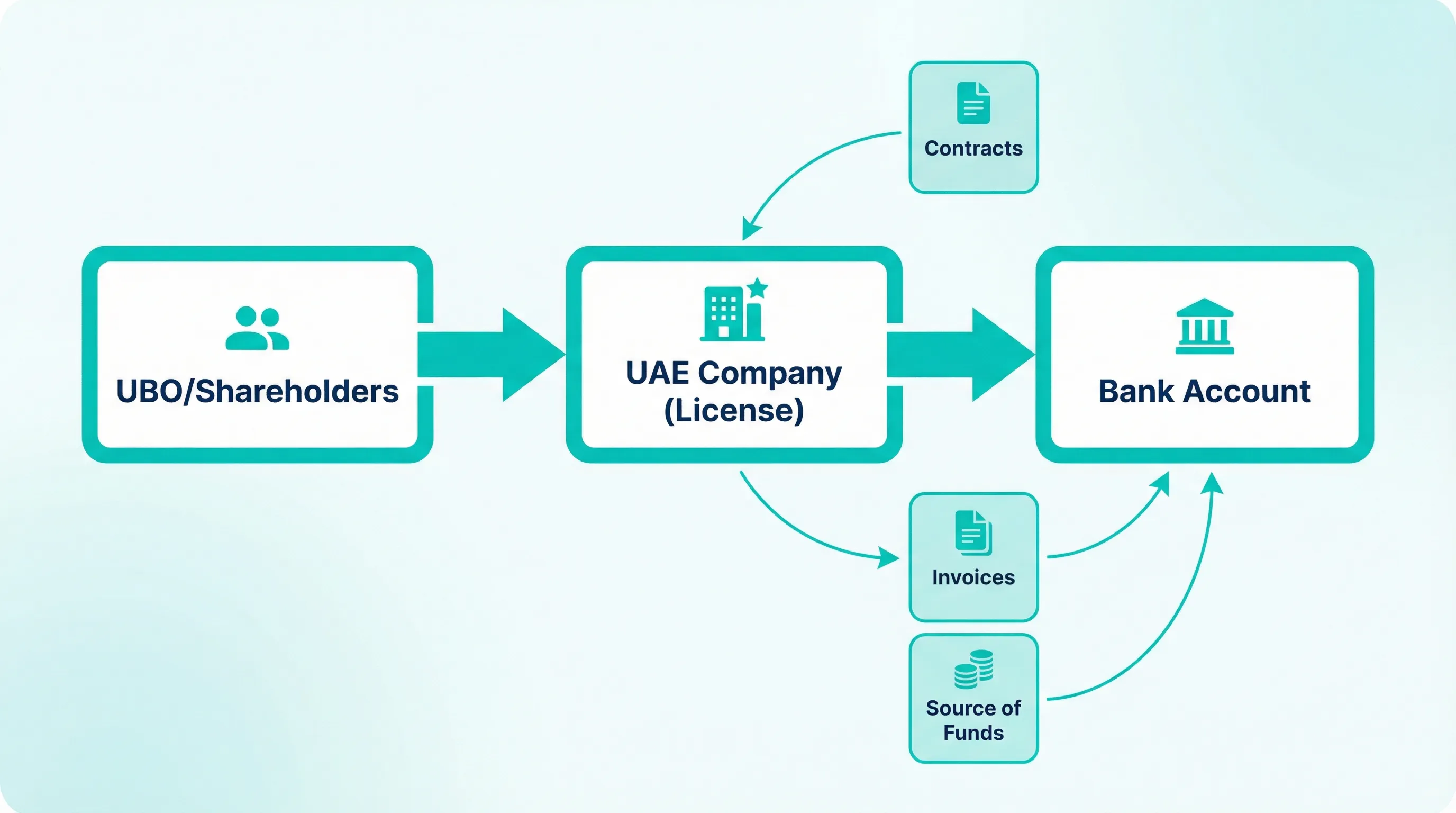

Source of funds and expected activity evidence

This is where many applications slow down. Prepare documents that explain the “why” and “how” of money movement:

- Bank statements (personal and or corporate, depending on profile)

- Contracts, invoices, purchase orders, or signed client agreements

- Supplier agreements, distribution contracts, or proof of inventory model

- A simple forecast of expected incoming/outgoing flows and countries

Requirements by bank type

Different bank types tend to apply different thresholds for what “good” looks like.

1) Local UAE banks (traditional domestic banks)

Best for: day-to-day UAE operations, local payments, WPS (where applicable), regional trade, and businesses that want a strong local banking relationship.

Typical requirements and focus areas:

- Clear alignment between license activity and real operations. If you are licensed for “general trading,” expect more questions than a narrow, well-explained service activity.

- Stronger emphasis on UAE substance. A lease, staff plans, local customers, or proof of operations can help.

- More detailed UBO review. If ownership includes holding companies or multiple jurisdictions, be ready with a clean org chart and supporting documents.

Common “extra asks” at this bank type:

- More extensive supporting documentation for first deposits and initial transactions

- Clarification of counterparties, especially cross-border

- In-person meeting with a signatory (varies by bank and profile)

2) International banks with UAE presence

Best for: multinational groups, companies with foreign parent entities, cross-border treasury flows, or founders who already bank internationally.

Typical requirements and focus areas:

- Higher documentation expectations for ownership chain, group structure, and governance.

- Greater scrutiny of cross-border payments (who you pay, why, and where).

- Preference for established track record (existing financials or a history in another jurisdiction can help).

If your business has overseas reporting obligations, it is smart to keep your compliance “paper trail” consistent across countries. For example, if you have US excise tax filing requirements, using an IRS-authorized Form 720 e-filing provider can help keep filings organized and timely, which supports a cleaner compliance narrative when banks request supporting information.

3) Digital banks and fintech business accounts

Best for: founders prioritizing speed, app-based onboarding, and straightforward account needs (collections, transfers, basic cards), especially early-stage companies.

Typical requirements and focus areas:

- Standardized onboarding and document checklists. Processes are often more structured and less relationship-driven.

- Clear beneficial ownership and simple structures tend to perform best.

- Defined use case. Digital banks often want a very clear explanation of expected activity (transaction volumes, countries, counterparties).

Important reality check: “Easier onboarding” does not mean “no compliance.” If the activity or structure triggers risk flags, digital providers can still request extensive evidence or decline.

4) Islamic banks

Best for: companies that prefer Sharia-compliant banking principles, or clients who already have relationships with Islamic banking groups.

Typical requirements and focus areas:

- Standard KYC and corporate documents (similar baseline to other banks).

- Additional review of the nature of the activity to ensure it is compatible with the bank’s policies.

If your activity involves financing models, certain trading categories, or sectors that require additional screening, expect more clarification questions.

Free Zone vs Mainland companies (what changes for account opening)

Banks can open accounts for both, but the evidence they expect may differ.

Free Zone companies:

- Banks often look closely at where the business is actually conducted (UAE vs overseas) and how counterparties are contracted.

- Some Free Zone setups rely on flexi-desks, which is common, but you may need stronger proof of operations (contracts, invoices, pipeline).

Mainland companies:

- Banks may expect more local operational linkage (local clients, office, hiring plans) depending on the activity.

What matters most is not the label “Free Zone” or “Mainland,” it is whether your documentation makes the business model unambiguous.

Higher-scrutiny activities: what to prepare upfront

Banks rarely reject “because they can’t,” they reject because the risk cannot be comfortably explained with the available evidence.

You may face extra scrutiny if your company involves:

- Complex international flows with limited local footprint

- Payment services, money services, or activities that resemble regulated financial services

- Crypto-related exposure (direct or indirect) depending on the bank’s internal policy

- High-volume trading with thin margins and many counterparties

In these cases, prepare:

- A one-page narrative of the business model (how you win business, deliver, and get paid)

- Signed contracts or clear proof of pipeline

- Counterparty samples (who pays you, who you pay)

- Source of funds and source of wealth evidence for beneficial owners

Common reasons applications get delayed or declined

Most failed applications come down to a small set of avoidable issues:

Inconsistencies across documents

If your license activity says one thing, your website says another, and the company profile suggests a third, compliance teams assume the worst.

Unclear ownership or control

If a UBO chart is missing, outdated, or doesn’t match the MOA/share register, you will lose weeks.

Weak explanation of funds

Banks want logic, not just paperwork. “Consulting” plus large incoming transfers from multiple unrelated entities with no contracts is a classic mismatch.

No operational story

New companies can open accounts, but you need to show you are building a real business (pipeline, proposals, signed agreements, professional background).

A realistic timeline (and how to shorten it)

Timeframes vary widely, but the process usually looks like this:

| Phase | What happens | How to reduce delays |

|---|---|---|

| Pre-check | Bank suitability based on activity, ownership, residency | Pick the right bank type for your profile before applying |

| Submission | Upload or deliver documents, complete forms | Submit a complete pack with consistent naming and dates |

| Compliance review | KYC, UBO, source of funds checks, questions | Answer fast, attach evidence, keep explanations simple |

| Approval and activation | Account opened, online banking set up | Ensure signatory availability and correct resolution wording |

The fastest wins usually come from (1) choosing the right bank for the profile and (2) submitting a complete, coherent file.

How structuring impacts bankability

Banks do not only evaluate your company, they evaluate the clarity of your corporate structure.

A bank-friendly structure is typically:

- Easy to explain (simple ownership chain)

- Easy to evidence (clean corporate documents for every entity in the chain)

- Consistent with the business model (substance, governance, realistic flows)

If you need nominee arrangements or complex holding structures for legitimate reasons, it becomes even more important to prepare governance documentation and a transparent narrative that a compliance team can approve.

Frequently Asked Questions

What is the minimum requirement to open a corporate bank account in the UAE? The baseline is a valid trade license plus complete company documents, UBO information, and KYC for owners and signatories. Most delays come from missing source-of-funds evidence and unclear business activity.

Can I open a UAE corporate bank account as a non-resident? Sometimes, yes, depending on the bank type and risk profile. Non-resident owners typically face additional KYC, stronger source-of-funds checks, and more scrutiny of UAE substance and counterparties.

Do Free Zone companies face more difficulty with bank account opening? Not inherently, but banks often ask Free Zone companies to clearly demonstrate where operations happen and provide stronger commercial evidence (contracts, invoices, pipeline), especially if business is mainly cross-border.

Why do banks ask for invoices or contracts if the company is new? Banks use commercial documents to verify the business model and expected transaction activity. If you are pre-revenue, a strong pipeline (proposals, signed LOIs, onboarding emails, supplier agreements) can help.

Which bank type is best for a newly formed UAE company? It depends on the activity, ownership, and expected flows. Digital providers may be faster for straightforward profiles, while traditional banks may be better if you need a long-term local relationship and broader services.

Need help choosing the right bank type and preparing an approval-ready file?

Alldren supports clients with UAE company setup, structuring, compliance, and bank account opening support, with transparent, upfront guidance and direct access to senior experts. If you want to reduce back-and-forth with compliance teams, align your corporate structure with your banking goals, and submit a clean application package, start here: Alldren.