Operating in the UAE has long been associated with straightforward taxation, but by 2026 “tax in the UAE” for companies is no longer a single-topic conversation. Corporate Tax is established, VAT remains a daily operational reality, and documentation expectations (accounting, transfer pricing, and record-keeping) are getting more rigorous. Add the phased introduction of e-invoicing and the question for most founders and finance teams becomes practical: what exactly do we need to do, by when, and how do we stay compliant without overpaying?

This guide breaks down Tax UAE considerations for companies in 2026, with a focus on what changes your actions, not just definitions.

Tax UAE in 2026: what applies to most companies

Most companies will deal with some combination of the following:

- UAE Corporate Tax (CT): applies to UAE juridical persons and certain individuals conducting business, with special regimes for qualifying free zone persons.

- VAT (Value Added Tax): 5% VAT with mandatory and voluntary registration thresholds.

- Excise Tax: relevant only if you produce, import, stockpile, or sell excise goods.

- Customs duties: relevant for importers and certain trading models.

The UAE still generally has:

- 0% withholding tax on domestic and cross-border payments (as currently legislated).

- No federal personal income tax on salary income.

For primary sources and definitions, use the official guidance from the UAE Ministry of Finance on Corporate Tax and the Federal Tax Authority for VAT:

- UAE Ministry of Finance, Corporate Tax

- Federal Tax Authority (FTA)

UAE Corporate Tax (CT) in 2026: the core rules businesses must understand

1) Who is subject to Corporate Tax?

In practice, Corporate Tax is relevant for:

- Mainland LLCs and other UAE incorporated entities.

- Many free zone companies, even if they may benefit from a 0% rate on qualifying income under the free zone regime.

- Foreign companies that are effectively managed and controlled in the UAE or have a taxable presence under the Corporate Tax law.

The exact analysis depends on your legal form, activities, license, where your management decisions are made, and whether you qualify for any special regime.

2) Corporate Tax rates (what most companies will see)

As a baseline, the UAE Corporate Tax system applies:

- 0% on taxable income up to AED 375,000.

- 9% on taxable income above AED 375,000.

Some large multinational groups may also be affected by global minimum tax developments (Pillar Two type rules) depending on how UAE implementing measures apply to them, but that is not the day-to-day situation for most SMEs.

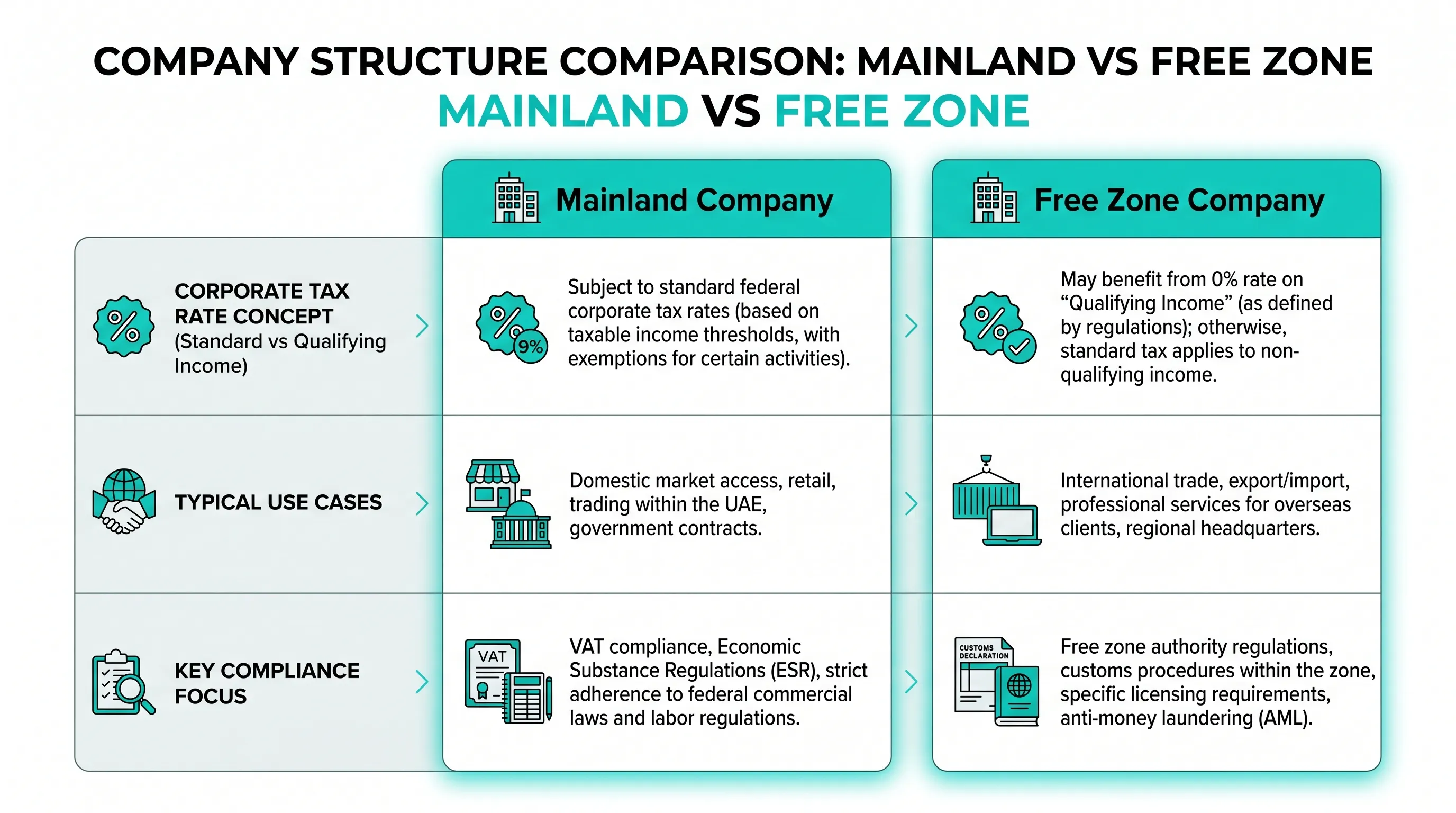

3) Free zone companies: 0% is possible, but it is not automatic

A free zone company can potentially access the 0% Corporate Tax rate on “qualifying income” if it meets the conditions to be a Qualifying Free Zone Person (QFZP) and follows the compliance requirements.

Key practical points for 2026:

- You still need strong substance and compliance practices (people, premises arrangements, governance, and documentation) aligned with your actual operating model.

- The split between qualifying income (potentially 0%) and non-qualifying income (potentially 9%) can matter. Your invoicing flows, customer locations, and activities need to match what your license and free zone framework allow.

- The “best” free zone is rarely about the headline rate, it is about whether your revenue model can stay within qualifying lanes without creating commercial friction.

If your business sells into the UAE mainland, works with UAE-based customers, or relies on onshore delivery teams, it is especially important to structure correctly from day one.

4) Small Business Relief: helpful, but eligibility matters

The UAE introduced Small Business Relief to simplify Corporate Tax for smaller businesses that meet specific criteria. In 2026, this relief can still be relevant for eligible companies (subject to the applicable Cabinet decisions and conditions for the relevant tax period).

Practical takeaway: do not assume you qualify just because you are “small.” Eligibility depends on measurable thresholds (not feelings), and group structures can change the analysis.

5) Accounting, records, and audit readiness

Corporate Tax compliance is not only about filing a return. It is also about being able to defend the numbers.

At a minimum, companies should treat the following as non-negotiable:

- Maintain complete accounting records and support for revenue and expenses.

- Ensure consistent bookkeeping (monthly is preferable, quarterly is often too slow for fast-growing SMEs).

- Keep contracts, invoices, bank statements, payroll records, and supporting schedules organized.

Even when an audit is not explicitly required for your license, tax filings can still be reviewed. If your numbers depend on management estimates or related-party pricing, documentation becomes even more important.

6) Corporate Tax timeline: registration, filing, and payments

While specific deadlines can depend on your facts, a common baseline is:

- Corporate Tax return filing is generally due within 9 months from the end of the relevant tax period.

Registration timelines can vary based on entity type and licensing, and the FTA has issued phased guidance in prior periods. The safest approach in 2026 is to confirm your obligations early and register on time based on the latest FTA instructions.

VAT in the UAE in 2026: the operational tax you feel every day

VAT often creates more day-to-day work than Corporate Tax because it touches invoicing, contracts, and collections.

VAT rate and thresholds (common cases)

- Standard VAT rate is 5%.

- Mandatory registration generally applies when taxable supplies exceed AED 375,000 over a 12-month period (or are expected to exceed it).

- Voluntary registration may be available from AED 187,500, subject to conditions.

Always validate your specific scenario against current FTA guidance, especially if you have:

- Mixed taxable and exempt supplies.

- Cross-border services.

- Marketplace or agency models.

- Complex “place of supply” questions.

VAT mistakes that commonly create penalties

In 2026, many UAE companies are past first-time VAT implementation issues, but several recurring risks remain:

- Charging VAT incorrectly (or failing to charge it when required).

- Recovering input VAT without proper tax invoices.

- Misclassifying exports and zero-rated supplies.

- Weak credit note and refund documentation.

- Treating deposits, retainers, and milestones inconsistently.

A practical way to reduce VAT errors is to standardize how your business issues invoices, approves tax invoices from suppliers, and tags transactions in your accounting system.

Excise tax and customs: only for some, but high impact when relevant

Excise tax

Excise tax applies to specific product categories (for example, certain tobacco products, vaping products, energy drinks, and sweetened beverages). If your business deals in these categories, excise compliance becomes a core function, not an afterthought.

Customs

If you import goods, your customs model affects:

- Landed cost and pricing strategy.

- Cash flow (timing of duties and VAT at import, where applicable).

- Documentation requirements (HS codes, commercial invoices, certificates of origin).

Trading companies often benefit from getting their end-to-end flows reviewed: supplier terms, incoterms, shipping documents, and how those map to VAT and customs declarations.

Transfer pricing in the UAE (2026): growing importance for groups and related parties

If your UAE company transacts with related parties (UAE or overseas), transfer pricing is a major Corporate Tax risk area.

Common related-party transactions include:

- Management fees.

- IP licensing.

- Intercompany loans.

- Cost-sharing and recharge arrangements.

- Buying and selling goods within a group.

The key principle is that related-party transactions should be priced on an arm’s length basis, supported by documentation. Even SMEs can be pulled into transfer pricing complexity if they expand internationally or restructure into multiple entities.

If you are building a group structure in the UAE, it is usually cheaper to design transfer pricing and intercompany contracts early than to “fix” them after the first tax filing.

E-invoicing in the UAE: why 2026 matters

The UAE has announced plans to implement an e-invoicing framework in phases. For operators, the impact is that invoice data requirements and system interoperability become compliance topics, not just accounting preferences.

What companies can do now (even before full rollout applies to them):

- Make sure your invoicing system can generate structured invoice data and store audit trails.

- Clean up master data (customer addresses, TRNs, product and service descriptions).

- Standardize invoice numbering, credit note processes, and tax invoice templates.

For official updates and implementation direction, monitor the UAE Ministry of Finance communications.

A practical 2026 compliance checklist (without overcomplicating it)

If you want a workable internal plan, focus on these pillars:

Corporate Tax readiness

- Confirm whether you are a mainland entity, free zone entity, or foreign entity with a UAE tax footprint.

- Decide whether your accounting records are strong enough to support a Corporate Tax return.

- Identify related-party transactions early and document them.

- Establish a close process for year-end adjustments and supporting schedules.

VAT hygiene

- Reconcile VAT returns to accounting monthly.

- Ensure tax invoices meet FTA requirements before claiming input VAT.

- Document zero-rating positions (especially exports and cross-border services).

Governance and substance

- Keep board resolutions and key decisions consistent with where the business is actually managed.

- Align licenses, activities, and contracts with how money is really earned.

The goal is not “perfect paperwork.” The goal is a structure and process that can be defended.

Tax UAE at a glance (2026)

| Tax type | Typical rate | Who it usually affects | Core action items |

|---|---|---|---|

| Corporate Tax | 0% up to AED 375,000 taxable income, 9% above | Most UAE companies (mainland and many free zone entities) | Register if required, keep accounting records, file CT return within deadlines |

| VAT | 5% | Businesses exceeding VAT thresholds, and many B2B operators | Register when required, issue compliant tax invoices, file VAT returns and maintain documentation |

| Excise Tax | Varies by product category | Businesses dealing in excise goods | Register, file excise returns, maintain product and stock records |

| Customs duty | Depends on goods and origin | Importers and trading companies | Correct HS classification, keep shipping docs, align incoterms and customs declarations |

When “tax optimization” becomes risky in the UAE

In 2026, aggressive tax positioning often fails in the same way: a structure that looks good on a diagram but does not match how the company actually operates.

Red flags that typically deserve a second look:

- Free zone entity claiming 0% treatment while most revenue is effectively onshore, without operational separation.

- Large management fees without clear services, deliverables, or benchmarks.

- Shareholder expenses run through the company without business rationale.

- Inconsistent contracts, invoices, and bank flows.

A conservative rule: if your structure depends on assumptions you cannot document, it is not a strategy, it is a liability.

How to choose the right setup for a tax-compliant UAE company

Because Corporate Tax now applies broadly, UAE entity choice is less about “tax vs no tax” and more about:

- What activities you perform and where.

- Whether you need access to the UAE mainland market.

- Whether your income can be treated as qualifying under free zone conditions.

- Your governance needs (investors, partners, holding structures).

- Your ability to maintain compliance: bookkeeping, VAT, substance, and documentation.

If you are still pre-incorporation, this is the best moment to plan. Fixing a misaligned structure later often costs more in re-licensing, banking friction, and remediation work.

Frequently Asked Questions

Does the UAE have corporate tax in 2026? Yes. UAE Corporate Tax is in force, with 0% on taxable income up to AED 375,000 and 9% above that threshold for most standard cases.

Do free zone companies pay 0% Corporate Tax automatically? No. Free zone companies may access a 0% rate on qualifying income if they meet the conditions to be a Qualifying Free Zone Person and follow the required compliance.

When is a Corporate Tax return due in the UAE? Corporate Tax returns are generally due within 9 months after the end of the relevant tax period (confirm your specific tax period and the latest FTA instructions).

When do I need to register for VAT in the UAE? Mandatory VAT registration generally applies once taxable supplies exceed AED 375,000 over a 12-month period (or are expected to). Voluntary registration may be possible from AED 187,500, subject to conditions.

Is withholding tax charged on payments from the UAE? The UAE Corporate Tax law provides for a 0% withholding tax rate in many cases. Always confirm treatment for your specific payment type and counterparties.

Get your UAE tax and structure right (without guesswork)

If you are setting up in the UAE or adapting to Corporate Tax in 2026, the highest ROI work is usually upfront: choosing the right entity and operating model, setting up clean bookkeeping and VAT processes, and making sure free zone or mainland positioning matches your real revenue flows.

Alldren provides expert-led, transparent support for UAE company setup, structuring, tax registration, compliance management, and ongoing governance, with direct access to senior experts. Learn more at Alldren.